Why Every Business Needs a Cost Attribution Model And How to Build One

Understanding where business expenses originate and how they impact profitability is no longer optional; it is essential. A well-structured cost attribution model provides clarity by linking costs to actual business activities, enabling leaders to manage resources with greater precision.

Have you ever taken a look at your monthly expenses and wondered, “Where is all this money actually going?” You’re not alone. Businesses of all sizes often face this exact dilemma. Budgets are set, reports are reviewed, but when it’s time to trace specific costs back to the departments, products, or initiatives that generated them, things can quickly become murky.

This isn’t just a finance problem, it’s a strategic one. When costs are not attributed, it is nearly impossible to make confident decisions about pricing, resourcing, or even growth strategy. That’s where a cost attribution model comes in.

A cost attribution model provides your business with a reliable framework for understanding why costs exist, where they originate, and who or what is responsible for them. More importantly, it helps you allocate expenses in a way that reflects actual business activity, rather than relying on gut feeling or rough estimates.

In this blog, we’ll explore why every business, from established enterprises to fast-growing startups, needs a clear cost attribution strategy.

What Is A Cost Attribution Model

A cost attribution model is a structured method used to assign business expenses to their actual source. It links costs to specific activities, departments, products, or customers based on measurable usage or contribution.

This model ensures that each cost is attributed to its specific cause. It moves away from spreading expenses evenly or using arbitrary percentages. Instead, it uses data to reflect how resources are consumed across the organization.

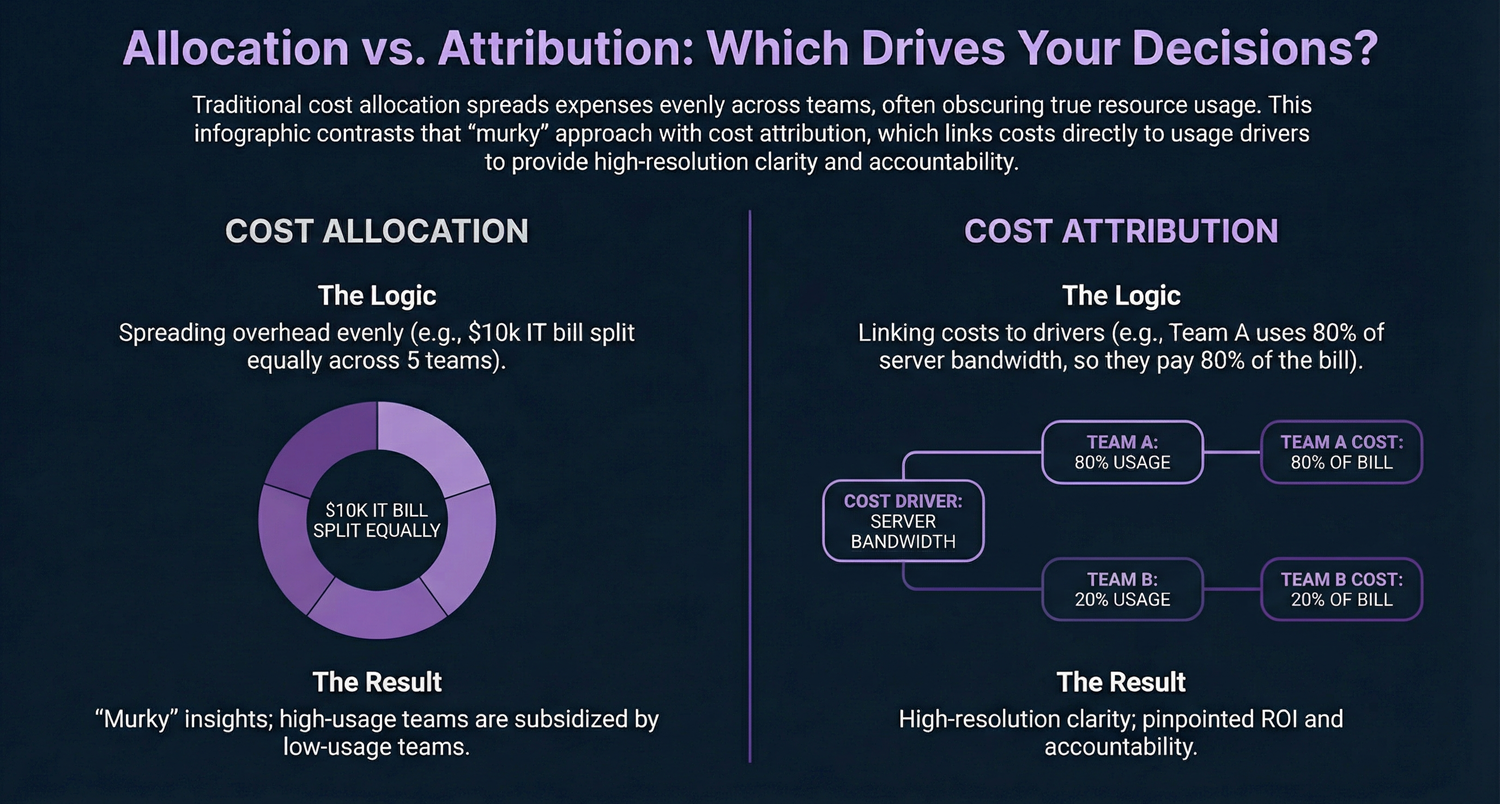

Cost attribution and cost allocation are often confused with each other. Cost allocation spreads costs across departments or units using simple formulas. These might include headcount or revenue share, regardless of actual usage.

Cost attribution focuses on identifying the real driver behind each expense. It uses specific data to assign costs with greater accuracy. This approach creates a more realistic picture of business operations and performance.

Modern businesses face increasing cost complexity. Cloud platforms, global teams, and subscription models have altered the behavior of costs. Traditional allocation methods fail to capture this complexity, resulting in inadequate financial insights.

The cost attribution model addresses this issue. It offers clarity in a landscape where shared resources, indirect costs, and variable usage are common. It helps organizations gain control, reduce waste, and make smarter financial decisions.

Why Cost Attribution Matters

Cost attribution enables data-driven decisions and better resource management.

- Informed decision-making:

- Accurate pricing:

- Resource optimization:

- Improved accountability:

Allocate costs based on actual usage.

Ensure prices reflect true costs.

Identify inefficiencies and reallocate resources.

Track costs to specific teams or activities.

Example:

Instead of equally sharing IT costs, a company assigns charges based on actual usage, ensuring each department pays fairly and improves budgeting.

Common Types Of Cost Attribution Models

Understanding which cost attribution model best suits your business operations is crucial for accurately allocating expenses and making informed, data-driven decisions. Each model offers a distinct approach to tracking and allocating costs, and selecting the right one can have substantial implications for financial planning, pricing strategies, and operational efficiency.

1. Direct Costing

Direct costing, also known as variable costing, only includes variable costs in calculating the cost of goods sold. These are costs that vary directly with production or service delivery, such as raw materials and labor directly associated with the production process. Fixed costs, such as rent or administrative salaries, are excluded from the cost structure in this model.

Key Features

- Allocates only variable costs to products or services, such as direct labor, raw materials, and manufacturing supplies.

- Excludes fixed costs such as overhead, utilities, and administrative costs.

- Provides a clearer view of how changes in production levels directly affect overall costs and profitability.

Best For: Direct costing is most beneficial for businesses focused on analyzing the immediate profitability of individual products or services based on their variable costs. It is particularly useful for short-term decision-making, such as evaluating whether to continue producing a product.

Why It Matters: This model helps businesses focus on operational efficiency and the marginal cost of production. By separating fixed and variable costs, companies can better understand how changes in production impact their bottom line. It is often used for decision-making regarding pricing, production volume, and cost control.

2. Absorption Costing

Absorption costing, also known as full costing, encompasses both fixed and variable costs in the calculation of the cost of goods sold. This method ensures that all costs, whether they change with production or not, are allocated to products or services. This model is commonly used for external financial reporting because it complies with accounting standards like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards).

Key Features

- Includes both fixed and variable costs in the cost of production, such as factory overhead, wages of administrative staff, and office rent.

- Used for external financial reporting and required for businesses to comply with standard accounting practices.

- Ensures that all production costs are accurately reflected in pricing, helping to avoid underpricing or overpricing of goods or services.

Best For: Businesses that need to produce comprehensive financial statements for external stakeholders, including investors, regulators, and auditors. It is also beneficial for companies seeking a comprehensive view of their total cost structure.

Why It Matters: Absorption costing ensures that every cost related to the production of goods or services is accounted for in the pricing structure. This helps businesses avoid miscalculations in pricing and ensures that they do not undercharge for their products or services, which could impact profitability.

3. Activity-Based Costing (ABC)

Activity-Based Costing (ABC) allocates costs based on the specific activities that drive those costs. Instead of applying a blanket allocation rate for overhead, ABC assigns costs to activities (e.g., production runs, customer support, or product design) based on the resources they consume. The idea is to identify and track each activity’s cost driver, like time or labor hours, to understand cost behavior better.

Key Features

- Assigns costs based on activities (e.g., machine setup, customer service, production runs) and cost drivers (e.g., labor hours, machine hours, or material usage).

- Provides granular insights into how resources are consumed across different activities.

- More accurate than traditional costing methods for businesses with complex production processes or diverse product lines.

Best For: ABC is particularly valuable for complex organizations with diverse activities or product lines that require a detailed breakdown of costs. This model is effective in identifying areas where inefficiencies or waste exist.

Why It Matters: ABC allows businesses to optimize resource allocation by pinpointing costly activities or underutilized resources. By focusing on cost drivers, businesses can refine their operations, eliminate non-value-added activities, and improve profitability through better cost management.

4. Time-Driven Activity-Based Costing (TDABC)

Time-Driven Activity-Based Costing (TDABC) is a streamlined version of traditional Activity-Based Costing (ABC). Rather than tracking multiple cost drivers, TDABC focuses on time as the central cost driver. In this model, costs are allocated based on the amount of time each activity consumes, thereby simplifying the cost allocation process.

Key Features

- Uses time as the primary cost driver for allocating costs.

- Simplifies data collection by focusing on time instead of multiple cost drivers.

- Allocates costs based on the resources used over a specific period, making it easier to implement than traditional Activity-Based Costing (ABC).

Best For: TDABC is best for businesses that perform repetitive tasks or activities, such as manufacturing or service-based companies with well-defined processes. It is also a good option for businesses looking for a simpler approach than traditional ABC.

Why It Matters: TDABC simplifies cost allocation without sacrificing accuracy. By focusing on time, businesses can make real-time decisions about process improvement and resource optimization. It is particularly useful for companies looking to scale operations while maintaining cost efficiency.

5. Fair Share/Equitable Allocation

Fair Share or Equitable Allocation is used when shared costs, such as office space, utilities, or IT services, need to be allocated across multiple departments or units. Rather than assigning costs based on specific activities, this model uses a predefined allocation base, such as revenue, headcount, or square footage, to determine costs.

Key Features

- Allocates shared costs using an equitable formula, such as headcount, revenue, or space usage.

- Often used for overhead costs or services that benefit multiple departments (e.g., IT support, office rent).

- Ensures that all departments contribute a fair share of the shared costs.

Best For: This model works well for organizations with centralized services that support multiple departments. It is particularly useful for companies that share common resources and want to allocate those costs fairly across all departments.

Why It Matters: Fair Share Allocation is important for transparency and accountability. By using a predefined formula, this method ensures that no department is unfairly burdened with shared costs. It promotes fairness and fosters collaboration among departments.

6. Step-Down Allocation

Step-Down Allocation is a method where service department costs are allocated to production departments or other service departments in a fixed order. The process starts with one department, and the costs are progressively allocated to others. This model is simpler than reciprocal allocation but does not fully account for the mutual services provided by service departments.

Key Features

- Allocates service department costs sequentially, starting with the first department and moving in a step-down order.

- Does not fully account for interdependencies between service departments, resulting in less accurate allocation compared to reciprocal allocation.

- Provides a simplified method for allocating indirect costs across departments.

Best For: Step-Down Allocation is ideal for businesses with a small number of service departments or those seeking a simpler approach to cost allocation. It is especially useful for organizations with clear and non-interdependent service functions.

Why It Matters: Step-Down Allocation is an efficient and cost-effective method for allocating service department costs. Though it may lack precision compared to other methods, it provides a good balance between simplicity and accuracy, making it a solid choice for many organizations.

Pro Tip- Selecting the appropriate cost attribution model depends on several key factors, including the complexity of your operations, the level of accuracy required for informed decision-making, and your business objectives. Understanding the strengths and limitations of each model enables you to make more informed decisions about cost allocation, which in turn enhances pricing strategies, resource optimization, and overall business profitability.

How to Build a Cost Attribution Model

Building an effective cost attribution model is crucial for businesses to allocate resources efficiently, set competitive pricing, and make data-driven decisions. Creating the right model involves understanding your business’s unique cost structure, choosing the appropriate attribution method, and continuously refining the model as your operations evolve.

1. Define Your Goals and Objectives

Before delving into the complexities of cost attribution, it is crucial to define the objectives of your model. Understand why you are building the model and how it aligns with your broader business objectives. These are the key questions you can adhere to:

- Are you trying to optimize resource allocation?

- Do you need a model for financial reporting or internal decision-making?

- Are you looking to enhance your pricing strategies?

2. Identify Cost Drivers

A cost driver is anything that causes a change in the cost of a business activity. Identifying the right cost drivers is the key to ensuring accurate cost allocation. Whether you use direct costs, activity-based costing, or another method, it is essential to identify the elements that directly impact your costs.

Key Considerations:

- For direct costing, focus on variable costs that change in proportion to production levels, such as raw materials and labor.

- For Activity-Based Costing (ABC), determine the activities that drive overhead costs, such as machine hours or customer interactions.

- For Absorption Costing, include both fixed and variable costs in your cost drivers to reflect the comprehensive cost structure.

3. Collect Data

Data collection is a crucial component of developing an accurate cost attribution model. Depending on the chosen model, you may need to collect data on direct costs, resource consumption, time spent on activities, or other key variables.

Data You May Need:

- Direct Costs:

- Indirect Costs:

- Activity Data:

Purchase invoices, employee payroll reports, labor tracking sheets, and material consumption logs.

Monthly utility statements, office lease agreements, software subscription records, and administrative staff salaries.

Number of customer service calls handled, total hours logged in production, frequency of machine usage, and volume of support tickets resolved.

4. Choose the Right Allocation Method

Once you have gathered sufficient data, select the cost attribution method that best aligns with your business needs and the available data. There are various models to choose from, each offering distinct advantages depending on the complexity of your business.

- If you are a manufacturing company with numerous overhead costs, Activity-Based Costing (ABC) may be more effective in accurately allocating indirect costs.

- If your business is focused on external financial reporting, Absorption Costing might be a better option, as it complies with regulatory standards like GAAP or IFRS.

- For service-based businesses, Fair Share Allocation might provide a fair distribution of overhead costs, ensuring that each department contributes proportionally.

5. Implement and Monitor the Model

After selecting your cost attribution model, implement it into your accounting or financial management system. This involves setting up the necessary processes, tools, and software to track, calculate, and allocate costs based on your model.

Implementation Steps

- Integrate the model into your enterprise resource planning (ERP) system or accounting software.

- Set up regular reviews and audits to ensure the model is functioning correctly and adjusting as required.

- Train employees on how the model works so that everyone in the organization understands how costs are being attributed.

6. Refine and Optimize

Cost attribution models are not static. As your business grows, markets evolve, or your operational structure changes, you may need to refine or optimize your cost attribution model. Regular updates will ensure the model remains aligned with your business needs.

Key Areas to Refine:

- Cost Drivers:

- Allocation Bases:

- Technology and Tools:

Reevaluate which activities or factors have the greatest impact on costs.

Adjust allocation bases as business activities evolve, such as changes in product mix or resource usage.

Leverage new tools, software, or data analytics solutions to improve the accuracy of cost allocation.

Key Takeaways

- A cost attribution model helps assign expenses to their true origin, improving financial clarity.

- It supports better pricing, resource planning, and strategic business decisions.

- Selecting the right model depends on your specific operations, data availability, and financial objectives.

- Continuous refinement ensures that your model evolves in tandem with business needs and market changes.

Conclusion

Cost attribution is not just a finance function; it is a strategic necessity. As businesses expand, the complexity of expenses increases. Without a clear method to connect costs to their source, organizations risk misallocating budgets, underpricing offerings, or missing critical growth opportunities.

Implementing the right cost attribution model empowers leaders to manage costs with precision, make confident decisions, and scale operations sustainably. When you can trace every dollar back to its purpose, you gain the insight needed to fuel growth and build lasting efficiency across your business.

Ready to turn your cost data into business intelligence? Let’s explore how cost attribution can support your next milestone.

Our experts at DiGGrowth can help you design and implement a cost attribution model tailored to your specific operations, providing clarity where it matters most and ensuring that every cost serves a strategic purpose. Reach out to us at info@diggrowth.com to start the conversation.

Ready to get started?

Increase your marketing ROI by 30% with custom dashboards & reports that present a clear picture of marketing effectiveness

Start Free Trial

Experience Premium Marketing Analytics At Budget-Friendly Pricing.

Learn how you can accurately measure return on marketing investment.

How Predictive AI Will Transform Paid Media Strategy in 2026

Paid media isn’t a channel game anymore, it’s...

Read full post post

Don’t Let AI Break Your Brand: What Every CMO Should Know

AI isn’t just another marketing tool. It’s changing...

Read full post post

From Demos to Deployment: Why MCP Is the Foundation of Agentic AI

A quiet revolution is unfolding in AI. And...

Read full post postFAQ's

Yes, even small businesses gain value from cost attribution. It helps them control spending, price accurately, and make data-informed decisions, especially as operations grow more complex.

A model should be reviewed quarterly or when significant operational changes occur. Regular updates ensure accuracy and alignment with current business processes, pricing, and resource use.

Not always. While software improves efficiency and accuracy, smaller businesses can start with spreadsheets. As complexity increases, automated tools become more valuable for tracking and analyzing cost data.

Common challenges include incomplete data, unclear cost drivers, and internal resistance. Addressing these requires cross-departmental collaboration, data transparency, and leadership support during implementation.

Yes. By identifying cost-heavy or resource-intensive activities, businesses can reduce waste, improve efficiency, and align operational decisions with environmental sustainability targets.